Credit score dropped overnight in Texas? Learn the exact reasons this happens and the fastest action plan Texans can use to recover their score.

The Texas-Sized Credit Score Shock

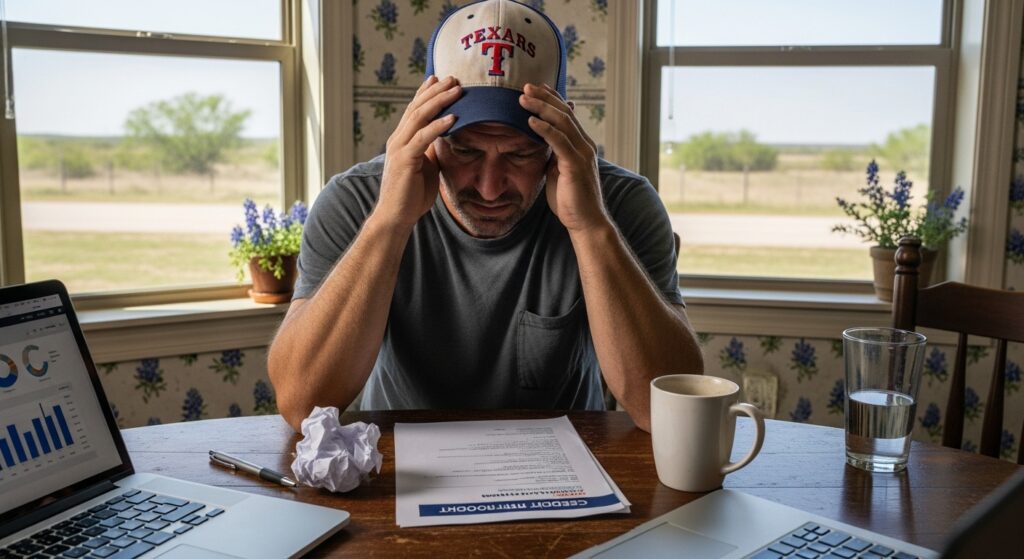

You check your credit score, a routine habit for the financially savvy. But this time, your stomach drops. Overnight, your score has plummeted by 30, 50, or even more points. Panic sets in. What happened? Was it fraud? A mistake? For Texas residents, this sudden drop isn’t just a number—it can feel like a threat to your ability to finance a home in a booming market, secure an auto loan with best rates, or simply manage your financial well-being.

Sudden credit score drops are one of the most common financial shocks reported by Texas consumers, especially during economic shifts and seasonal billing cycles.

The truth is, credit scores don’t drop without reason, even if the reason isn’t immediately obvious. In Texas, unique factors like the state’s economic landscape, specific lending practices, and even natural disasters can play a role. This guide is your definitive Texas roadmap. We’ll uncover the specific, often surprising, reasons your credit score tanked overnight and provide a clear, step-by-step plan tailored for Texans to not only diagnose the issue but fix it and rebuild stronger than ever. Your road to recovery starts here.

What Is a Credit Score and How Does It Actually Work?

Think of your credit score as your financial GPA, a three-digit number (typically FICO or VantageScore) that lenders use to gauge your risk as a borrower. In Texas, with its no-state-income-tax but higher property tax environment, your credit score directly impacts your wallet—from your mortgage rate in Houston to your APR on a truck loan in Dallas.

Scores are calculated using five main factors, but a sudden drop points to a recent, significant change in one of them:

- Payment History (35%): The kingpin. A single 30-day late payment can slash a good score.

- Credit Utilization (30%): How much credit you’re using vs. your total limits. Exceeding 30% on a card, or across all cards, hurts badly.

- Credit Age (15%): The average age of your accounts. Closing an old account can cause a dip.

- Credit Mix (10%): The variety of accounts (credit cards, loans, mortgage).

- New Credit (10%): Hard inquiries from applying for credit. Too many in a short span is a red flag.

An “overnight” drop is usually triggered when new data is reported to the three nationwide credit bureaus (Experian, Equifax, TransUnion) by your lenders, typically at the end of a billing cycle.

Why Did MY Credit Score Drop Overnight in Texas? The Top Culprits

Let’s diagnose the Texas-specific and common reasons. One of these is likely the culprit.

The Most Common Reasons for a Sudden Credit Score Drop

1. A Late Payment Was Reported: This is the biggest hitter. Even one 30-day-late mark can cause a massive drop, especially if you had a pristine history. Texas lenders are quick to report delinquencies.

2. Your Credit Utilization Spiked: Did you make a large purchase on a card? Did a lender decrease your credit limit (a common practice during economic uncertainty)? If your balance suddenly looks larger relative to your limit, your score will fall.

3. You Became an Authorized User… and Got Burned: If you were added to someone’s card to help build credit, their missteps (high balance, late payment) now hurt your report. Conversely, being removed from a positive account can also lower your score.

4. A Hard Inquiry from a New Application: Each application for credit (credit card, auto loan, personal loan) triggers a hard inquiry, knocking off a few points. Shopping for a mortgage or auto loan within a 14-45 day window usually counts as one inquiry, but applying for multiple credit cards will compound the damage.

Texas-Specific Factors That Can Crater Your Score

5. The “Texas Disaster Effect“: Hurricanes, floods, and winter storms can lead to missed payments due to displacement or income loss. While forbearance programs exist, miscommunication with lenders can still lead to negative reporting. Pro Tip: Federal disaster declarations often come with special consumer protections—act quickly if you’re affected.

6. Energy Bill Reporting Changes: Texas’s unique, deregulated energy market means your electric provider may report payment history to credit bureaus. Switching providers or a missed payment on a high summer bill could now show up.

7. Property Tax Liens and Public Records: Texas has some of the highest property taxes in the nation. An unpaid property tax bill can result in a tax lien, which is a severe negative mark on your credit report. Similarly, medical debt from a Texas hospital can end up in collections and on your report.

8. The “Rapid Rescoring” Glitch: If you or a lender used rapid rescoring to quickly update your report after fixing an error (common during home buying), sometimes the mechanics of this process can cause a temporary, confusing fluctuation.

The Immediate Fix-It Plan for Texas Residents

Don’t panic. Take systematic, documented action.

Step 1: Get the Real Story – Check Your Reports. Go to AnnualCreditReport.com and get your free reports from all three bureaus. Scrutinize every account for errors, unfamiliar accounts (identity theft), or recently reported late payments.

Step 2: Dispute Errors Immediately. Under federal law, you can dispute inaccuracies. Use the credit bureau’s online portal and send a certified letter to the lender. Texas law also provides consumer protections; document everything.

Step 3: Address Legitimate Negative Items.

- For Late Payments: Call the lender. If you have a good history, ask for a “goodwill adjustment.” Explain the situation (a Texas storm, an oversight) and request they remove the late payment as a courtesy.

- For High Utilization: Pay down balances below 30%, ideally below 10%. Consider a debt consolidation loan with low interest to simplify payments.

- For Collections: Negotiate a “pay-for-delete” agreement in writing before paying. They may agree to remove the collection from your report in exchange for payment.

Step 4: Build Positive Credit.

- Become an Authorized User on a family member’s well-managed credit card.

- Apply for a Secured Credit Card if your score is very low. It reports positively to all bureaus.

- Consider a Credit-Builder Loan from a local Texas credit union.

Fast-Track Solutions: When You Need Credit Now in Texas

If your drop has blocked you from essential financing, know your options. Online lenders often have more flexible requirements than big banks.

- For Immediate Needs: Look into lenders offering same day funding or instant approval on personal loans. Warning: These often come with higher rates, especially for those with bad credit.

- For Auto Financing: Texas is a zero down car loan market. Specialized online lenders and some dealerships work with top lenders for high approval chances, even with recent score drops. No credit check offers exist but beware of predatory terms.

- Rebuilding Tools: Use pre-qualification tools (soft inquiries) from lenders to see your potential rates without further harming your score.

Comparing Your Texas Rebuilding Options

| Option | Best For | Speed | Impact on Score | Texas Tip |

|---|---|---|---|---|

| DIY Dispute & Paydown | Long-term, sustainable repair | Slow (30-90 days) | High, lasting | Use Texas DFPS or AG resources for help. |

| Credit Counseling | Overwhelming debt, need structure | Medium | Positive with plan | Seek non-profit agencies approved by the TX AG. |

| Debt Consolidation Loan | High-interest credit card debt | Fast (1-7 days) | Can help utilization | Compare online lenders for best rates vs. local banks. |

| Secured Credit Card | No/bad credit, starting over | Fast approval | High with good use | Choose one that converts to unsecured and reports to all 3 bureaus. |

Protecting Your Texas Credit Score Long-Term

- Set Up Automatic Payments: Avoid late payments forever.

- Use Credit Monitoring: Many banks and free services offer alerts for score changes or new inquiries.

- Keep Old Accounts Open: Maintain your credit history length.

- Be Strategic with Applications: Space out credit inquiries. Only apply for what you need.

Frequently Asked Questions (FAQ) for Texans

Q: How long will it take to recover my credit score in Texas?

A: It depends on the cause. A single high balance can rebound in 1-2 billing cycles. A late payment or collection account can hurt for up to 7 years, but its impact lessens significantly after 2 years. Consistent good behavior is key.

Q: Are there “quick fix” credit repair companies in Texas I should use?

A: Be extremely cautious. Many charge high fees for services you can do yourself (like disputing errors). Texas has laws regulating credit services organizations. Always research and know your rights before signing anything.

Q: Can my Texas electric bill really affect my credit?

A: Yes. While not all providers report to credit bureaus, an unpaid bill that goes to collections absolutely will appear on your credit report and damage your score.

Q: I was affected by a hurricane and missed payments. What can I do?

A: Contact your lenders and servicers immediately. Federal disaster declarations often trigger forbearance or relief programs. Get all agreements in writing to ensure they do not report the paused payments as delinquent.

Q: Where can I get free, trusted help with credit issues in Texas?

A: Non-profit credit counseling agencies approved by the Texas Attorney General (like Apprisen or GreenPath) offer free or low-cost advice. The Texas Department of Banking and the Office of Consumer Credit Commissioner are also resources.

Take Control of Your Texas Financial Future

A sudden credit score drop in Texas is a setback, not a life sentence. By understanding the unique Texas factors at play—from disaster impacts to energy bills—and taking the precise, proactive steps outlined here, you can diagnose the problem, fix the damage, and rebuild a score that opens doors.

The most powerful step is the next one. Don’t let uncertainty paralyze you. Most credit score drops can be partially reversed within 30 to 60 days if the right steps are taken early

Our Fact Checking Process

Priorizamos precisão e integridade em nosso conteúdo. Veja como mantemos altos padrões:- Revisão de especialistas: todos os artigos são revisados por especialistas no assunto.

- Validação da fonte: as informações são respaldadas por fontes confiáveis e atualizadas.

- Transparência: citamos referências claramente e divulgamos potenciais conflitos.

Our Review Board

Nosso conteúdo é cuidadosamente revisado por profissionais experientes para garantir precisão e relevância.- Especialistas qualificados: cada artigo é avaliado por especialistas com conhecimento específico da área.

- Insights atualizados: incorporamos as últimas pesquisas, tendências e padrões.

- Compromisso com a qualidade: os revisores garantem clareza, correção e integridade.